In 2015, there were a total of 47,149 vehicle crashes in Montana, according to the National Highway Traffic Safety Administration. For many of these crashes, there were multiple injured victims.

No one plans on being injured in an automobile accident. Unfortunately, serious crashes happen every day and even crashes that may seem minor as a passerby can result in significant damages and hardships for those involved. Even those who are injured victims in these crashes may not know how serious their injuries may be. For these reasons, it is crucial that you have adequate automobile insurance coverage to protect not only yourself, but others as well. Understanding your automobile insurance policy and the coverages available to you is crucial.

UNINSURED (UI) & UNDERINSURED (UIM) COVERAGE – Protection for yourself if another person is at-fault

Montana Law requires you to have minimum liability insurance to protect others. But, it is your responsibility to make sure you have adequate insurance to protect yourself in the event that other drivers do not have any or enough insurance to protect you. This includes paying for your damages in the unfortunate event you are a victim of an automobile accident.

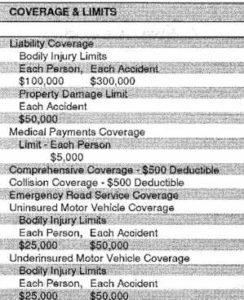

We cannot emphasize enough how important it is for consumers to have adequate uninsured and underinsured (UI/UIM) motorist coverage on their motor vehicles. While Montana law requires $25,000 per person and $50,000 per occurrence liability bodily injury coverage (protection for victims of an at-fault driver), this coverage is all too often inadequate. And, in some cases people still choose to drive without the required insurance.

If you choose to decline uninsured or underinsured (UI/UIM) motorist coverage, you are leaving yourself extremely vulnerable and without the coverage you will need if you are the victim of a collision. A Montana Legislative Audit Committee estimated approximately 9-15% of all motor vehicles registered in Montana are operated without liability insurance. Many, many more are operated with only the minimum liability insurance which is often woefully inadequate when serious injury crashes occur.

A scenario of uninsured and underinsured: Don’t let this be you

It’s time to renew your automobile insurance policy and to save money you reject uninsured and underinsured motorist coverage. You also reject medical payments “med-pay” coverage.

During the policy period you are driving with your spouse and your two children in your vehicle and a negligent driver crosses the center line and impacts your vehicle head-on at 45 miles per hour. You, your spouse and your two children are taken to the nearest emergency department by ambulance. You and your passengers are treated by the emergency doctors, x-rays are taken, MRIs and CT scans may be needed, and medications are prescribed for pain. You and your family will require follow-up care by a physician and, depending on your injuries, months and very likely years of treatment will follow.

You and your spouse are unable to work for a significant period of time as a result of your injuries and for weeks you are also unable to care for your children and their injuries because you are in pain and injured. You have to rely on others to help with everyday tasks such as cleaning and grocery shopping. You have no wages coming in because you are injured and unable to work. Your mortgage or rent is due. Your utilities are due. Medical bills are arriving in the mail. You receive a bill from the hospital that is tens of thousands of dollars. Bills keep piling up.

Then, you find out that the person who caused the collision only carried the minimum liability coverage required by Montana Law — $25,000/$50,000 Bodily Injury

What does this mean for you? This means that there is $50,000 of insurance coverage available to split between your four family members AND those funds also have to be divided between any passengers that may have been in the car of the person who hit you if those persons suffered injuries.

This is a situation none of us want to find ourselves in.

You can’t afford not to have uninsured or underinsured insurance coverage.

Medical Payments Coverage (“Med-Pay”)

Medical Payments Coverage is often referred to as “Med-Pay” coverage. This insurance coverage is an optional coverage you can purchase on your automobile insurance policy. It is a “no fault” coverage which means it covers your medical expenses in the event of an automobile accident, no matter who is at fault for the collision.

Med-pay insurance also covers you when you are in a vehicle other than your own and if you are a pedestrian struck by a motor vehicle. Med-Pay coverage provides payment for reasonable expenses incurred for necessary medical and funeral services resulting from bodily injury to an insured resulting from an accident.

Medical Payments Coverage applies to any named insured or any family member while occupying a covered vehicle or as a pedestrian when struck by a motor vehicle. Med-Pay also provides coverage to a person occupying a covered vehicle or a motor vehicle operated by an insured or the family member if the vehicle is a private passenger automobile.

PROTECTION FOR OTHERS IF YOU ARE AT-FAULT

Bodily Injury Liability

Bodily injury liability coverage protects you financially when you are at-fault in a motor vehicle collision that results in personal injuries to others. Bodily injury insurance coverage pays for medical expenses, funeral costs, pain and suffering, lost income, and other damages to those who are the victims of a collision. Bodily injury coverage does not pay for damages of the person who caused the collision.

Montana law requires that any motor vehicle operated on public roads has a bodily injury liability insurance policy with minimum coverage of $25,000 for bodily injury or death of one person in any one accident and $50,000 because of bodily injury to or death of two or more persons in any one accident.

When you purchase motor vehicle insurance, your policy will include two different numbers – it may look something like this: Bodily Injury Liability Each Person/Each Occurrence $25,000/$50,000. This is because your policy includes two limits, a per person limit and a per accident limit. The per person limit is the maximum amount your insurance will pay for bodily injury to any one person. The per accident limit is the maximum amount your insurance will pay for bodily injury if multiple people have damages resulting from the accident.

Bodily injury is specifically defined in your auto insurance policy and the specific provisions regarding what is and is not covered will be defined in the policy language.

STACKING POLICIES

Under Montana Law, some automobile insurance policies such as uninsured motorist coverage (UM), underinsured motorist coverage (UIM) and medical payments coverage (“med-pay”) can be “stacked.” This means that similar insurance coverages can be added together to provide more insurance coverage. However, in order for you to be able to stack insurance coverages certain provisions must be met. Stacking policies can be complex and requires knowledge of Montana’s laws related to this matter. To determine whether your policies can be stacked, Paoli Law Firm can review your insurance policies, the premiums you paid, the number of vehicles you insure, and Montana Law.

Call Paoli Law Firm to request a free consultation at 406-542-3330.